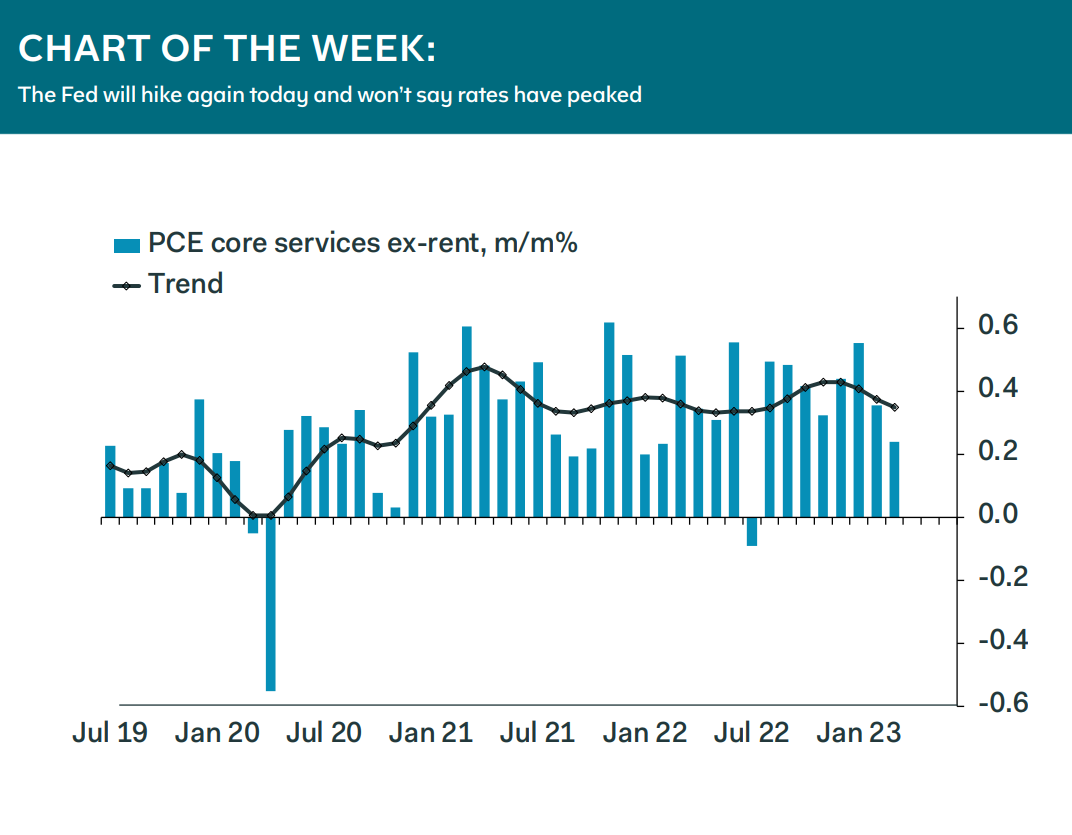

The Fed will raise rates by 25bp today, taking the mid-point of the range to 5.125%, just a hair below the 5.25% peak before the crash of 2008. We aren’t suggesting that a similar crash is imminent now, but the failure of three major banks in quick succession is a pretty good indication that monetary policy is already too tight. The Fed, however, remains focussed on the current inflation and activity data— including the core services PCE, shown in our chart of the week, which hasn’t slowed as much as they would like—paying only lip service to the idea that their previous actions will depress economic growth and inflation after a lag.

Accordingly, they won’t start to cut rates until it becomes clear from the activity and inflation data that the economy is headed clearly in the direction they want to see. We hope that evidence will emerge in time for the June meeting, by which time two rounds of labor market and CPI/PPI will have been released, but we can’t yet be certain. Leading indicators point to sharply slower payroll growth and lower inflation, but the noise-to-signal ratio in the monthly macro data is high. Across two months, just about anything can happen, and we cannot rule out a further increase in rates.

Ian Shepherdson, Chief Economist