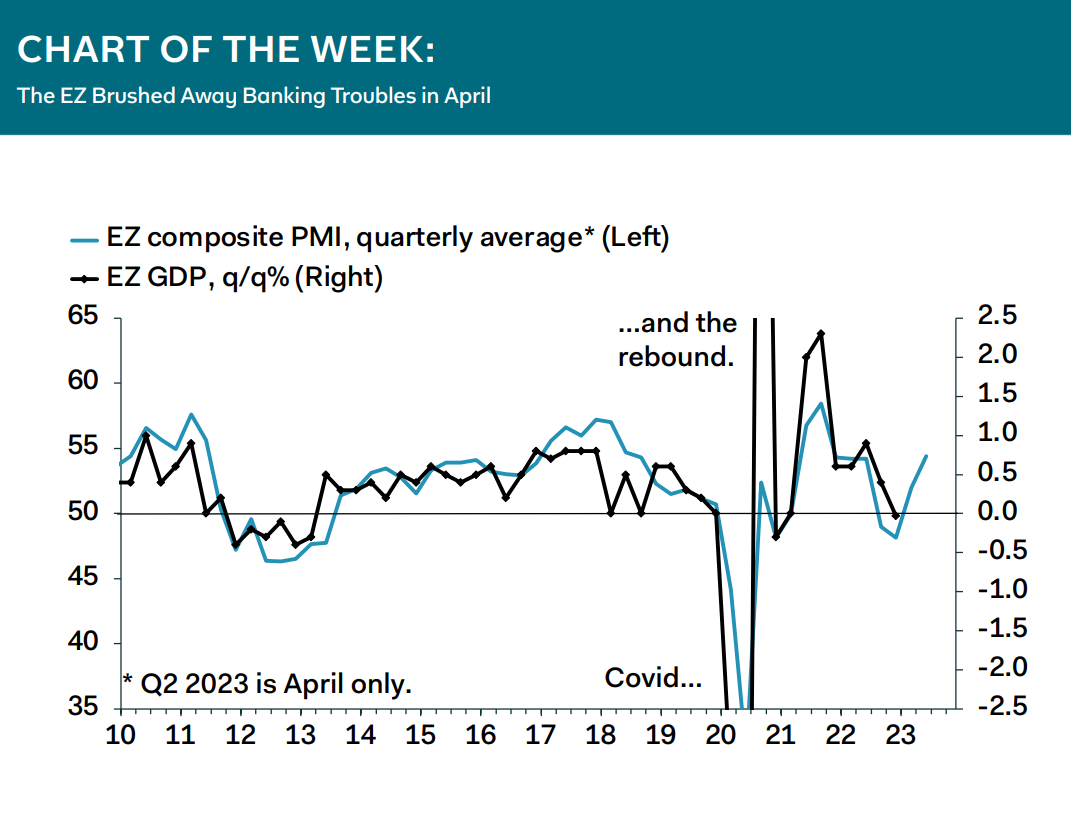

The jump in the EZ composite PMI in April—to an 11-month high of 54.4, from 53.7 in March—suggests that our forecast for GDP growth to remain lacklustre in Q2 is too modest. But

leading indicators still point to activity easing over the coming six-to-nine months, consistent

with a probable tightening in bank lending standards. We find it hard to believe slower

lending growth will leave investment unscathed in the next six months. Accordingly, we need to see the hard data before revising up our Q2 GDP call, just as we are now keenly waiting to see the next bank lending survey. Clearly, however, the PMI has put us on notice.

Meanwhile, still-elevated price indices add to the evidence that profit margin expansion is keeping a floor under inflation. The continued rapid increase in output prices, a still-resilient

labour market and signs the economy is so far taking monetary tightening and banking turmoil in its stride, add to our conviction that the central bank will hike by 50bp in May. It also increases the probability that the ECB will hike past May, taking the deposit rate to 4.0% or beyond.

Claus Vistesen, Chief Eurozone Economist