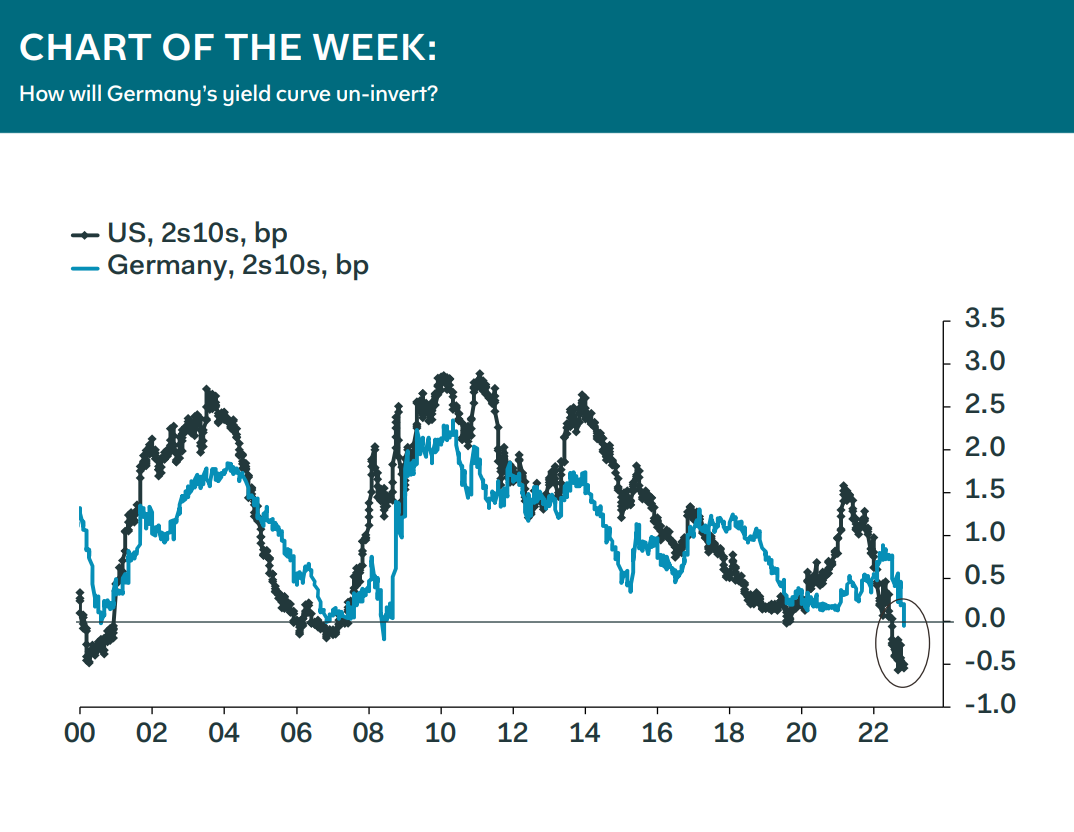

The German 2s10s yield curve inverted last week, a shift mainly driven by a sustained rise in two-year yields as the front-end has adjusted to a world with an ECB policy rate of 2% and above. Past experience indicates that the yield curve inversion will be fleeting, and that it will be resolved primarily by a reversal of monetary tightening as growth slows. We think this time is different.

Specifically, we think the curve will invert further, as the 10-year yield meanders sideways, while the two-year yield climbs further, in line with an ECB terminal rate of 2.5-to-3.0%. We then think the yield curve will un-invert via a sell-off in bunds, as 10-year yields hit 2.5%.

This is because: we think the ECB deposit rate will rise to 2.5% by March; that the two-year yield will settle 10-to-20bp below the deposit rate in line with the pre-Covid trend; and, EZ GDP growth

will re-accelerate in Q2 next year, pointing to a rebound in bund yields.

Claus Vistesen, Chief Eurozone Economist