INDEPENDENT, INCISIVE, ILLUMINATING

Welcome to Pantheon Macroeconomics

Pantheon Macroeconomics aims to be the premier provider of unbiased, independent, timely economic intelligence to financial market professionals around the world.

We provide actionable analysis in our research, which is published daily and is available by subscription. Our readers include banks, hedge funds, pension funds, insurance companies, family offices and specialist investors in property and other assets. Our publications are written for non-economists in an accessible, jargon-free style.

Our independent research tells investors only what they need to know. We keep it short and to the point, because your time is valuable. Our analysis is clear and objective, and we’re always happy to engage with readers who want more detail. Our daily Monitors cover the ground in just two pages, augmented by intraday Datanotes on key events.

What our clients say about us

Our U.S. coverage focuses on the key data which drive Federal Reserve policy decisions. We track the labor market, inflation, economic growth and financial market developments daily, filtering out the noise from the signal. We set out clearly our views on the path of the economy and the Fed’s likely response.

Our coverage focuses on the EZ economy as a whole, detailed coverage of the four major economies, and Switzerland. We also provide in-depth analysis of policy decisions by the ECB and SNB, and the region’s key asset markets. We focus on forward-looking data and always put our analysis into a relevant market context. We recognise the Eurozone’s structural challenges - incomplete monetary union and a rapidly ageing population - but we stress that this story is separate from the cyclical developments.

Our U.K. Service examines the outlook for interest rates, gilt yields and sterling. We scrutinise inflation, economic growth, fiscal policy and the labour and housing markets and their implications for monetary policy. The likely form and impact of brexit also is monitored closely. Samuel Tombs has spent nearly a decade exclusively analysing the U.K. Economy.

Our China+ service decodes the Chinese data, unveiling what’s really going on, and providing proprietary estimates of key statistics such as real GDP growth. On this groundwork, we are able to build high-conviction forecasts, with liquidity trends and PBoC action featuring highly. The service includes timely coverage of Japanese GDP and CPI, and valuable analysis of Korean exports as a bellwether for global trade. Our BoJ and BoK watch reports offer incisive previews and coverage of the main events and their implications.

Our Emerging Asia service tracks India and the fastest-growing economies in ASEAN, which as a bloc is the world’s fifth largest economy. Specifically, we will keep you abreast of developments in Indonesia, the Philippines, Thailand and Vietnam. Not only are these the next frontiers for global trade in the post-crisis period, but they also represent some of the biggest untapped consumer markets. The service includes analysis and forecasts for key macroeconomic indicators, as well as the outlook for FX and monetary policy.

We track the major economies in the region, focussing on Mexico, Brazil, Chile, Argentina, Colombia, Peru and Venezuela. We keep you up to date with both economic and political developments, with a close eye on the implications for currencies and central bank policy. Our Chief LatAm economist, Andres Abadia, is Colombian and a native Spanish speaker, so we go straight to the primary sources.

Our Specialist Team

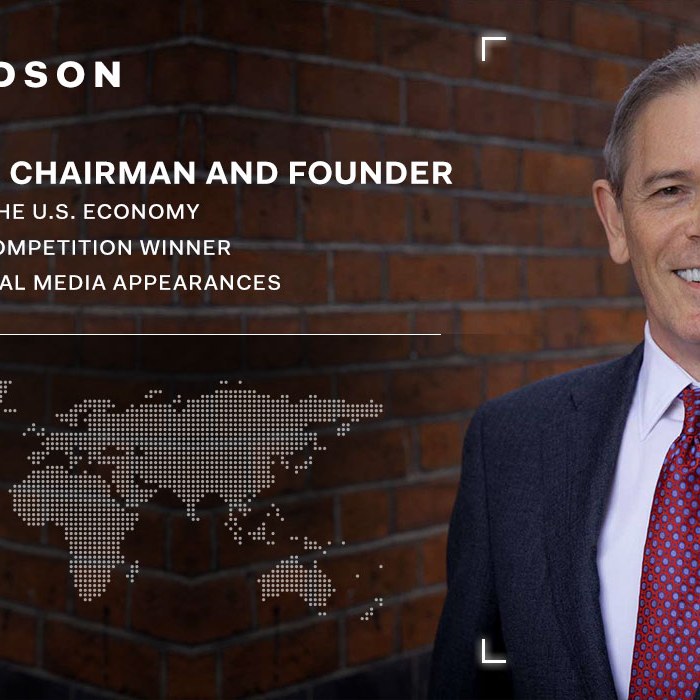

Ian Shepherdson's mission is to present complex economic ideas in a clear, understandable and actionable manner to financial market professionals. He has worked in and around financial markets for more than 25 years, developing a strong sense for what is important to investors, traders, salespeople and risk managers. Connect:

Samuel Tombs has won multiple awards for his UK forecasts. He had the highest average forecast score in Bloomberg’s 2021 panel, and Refinitiv ranked him the most accurate UK forecaster in 2020. He topped the annual ranking of forecasters for the UK economy compiled by the Sunday Times in 2014 and 2018, and was tied for first place in 2019.Connect:

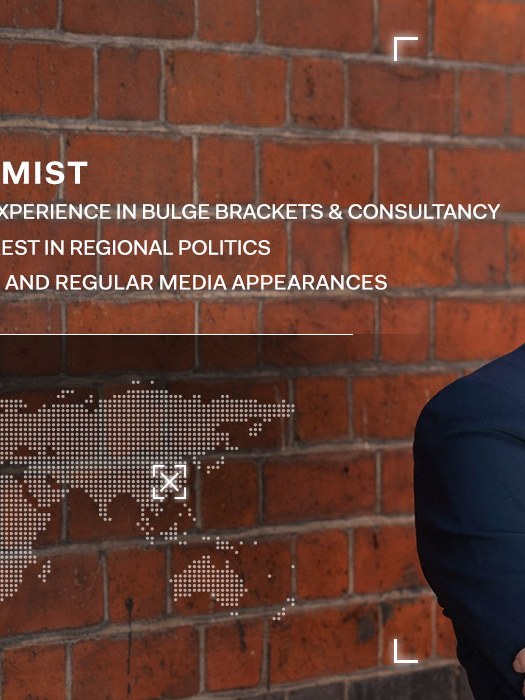

Rob Wood topped the Sunday Times annual ranking of forecasters for the UK economy in 2020, and has earned plaudits for his forecasting of inflation, the housing market, monetary policy, and consumer behaviour. He is extensively quoted in the press and has presented at a wide range of conferences, most recently the Bank of England Watcher’s Conference in late 2023. Connect:

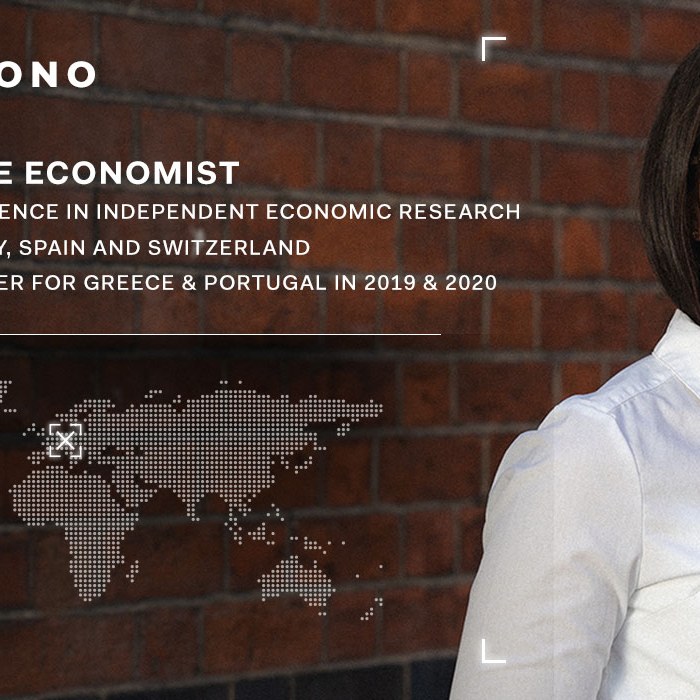

Claus Vistesen has several years' experience in the independent macro research space, as a freelancer, consultant and, latterly, as Head of Research of Variant Perception, Inc. He holds Master's degrees in economics and finance from the Copenhagen Business School and the University of Hull. Connect:

Duncan produces the China+ Service for Pantheon, covering China, Japan and Korea. He was previously Chief Strategist at Everbright Securities International, with a focus on China economic policy research. Before that he worked as an economist at Shui On Land, a property developer headquartered in Shanghai. Connect:

Miguel Chanco produces Pantheon’s Emerging Asia service, having covered several parts of the region for over ten years. He was previously the Lead Analyst for ASEAN at the Economist Intelligence Unit. Prior to that role, Miguel focused on India and frontier markets in South Asia for Capital Economics and Fitch Solutions (previously BMI Research). Connect:

Andres Abadia, who authors our Latin American service, was previously Head of Research at Bankia in Madrid. Andres is a native of Colombia and has wide and deep experience covering all the Latin American economies. He has degrees in Economics from the Universidad Autónoma de Madrid, Spain and the Universidad Externado de Colombia. Connect: